Research

18 May 2022

Shoppers are returning to pre-pandemic habits

The Tradeswell InFORM Report provides data on consumer demand for the first quarter of 2022.

(Illustration by Tradeswell)

Welcome to Data File. In this weekly feature, The Current shares key findings shaping the ecommerce landscape. This week, we're sharing a section from Tradeswell's InFORM Report Q1 2022, which provides insights on ecommerce finance, operations, retail and marketing. Download the full report here.

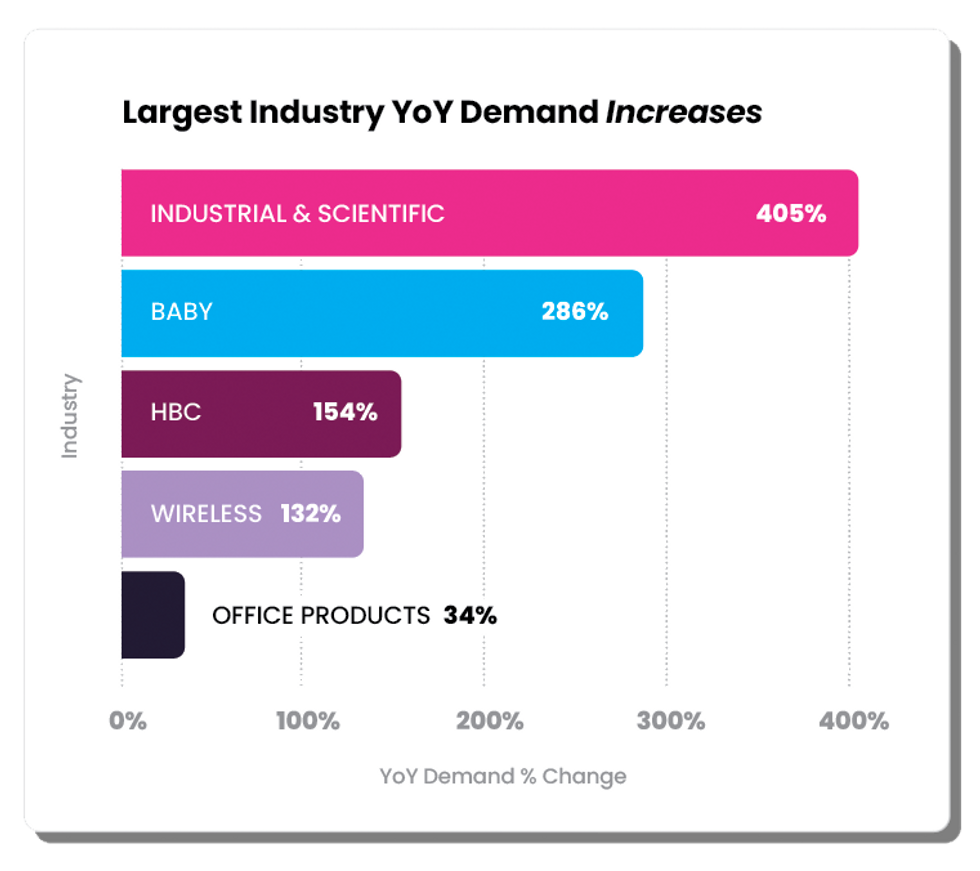

We broke down our consumer demand metric based on industries with the largest demand growth and decline. Investigating consumer demand trends allows you to understand how shoppers are shifting their buying habits, better predict sales, and make informed decisions around advertising and inventory.

Based on search term rankings and the volume of search terms, we identified the industries with the largest growth and decreases in consumer demand, along with how shopping trends are pivoting, as we emerge from the pandemic.

The Industrial and Scientific category, which includes rapid COVID tests and face masks, had the highest YoY growth rate from Q1 2021 to Q1 2022 at 405%. This correlates with COVID infection patterns. January 2022 saw the highest spike in COVID cases, likely causing the increased demand for tests and masks. Baby is another category that increased in consumer demand with a 286% increase in growth YoY in Q1 2022. Early in the pandemic, many experts believed there would be a baby boom with more people staying home. Instead, birth rates dropped in 2020. Based on our data and supporting outside research, we expect to see a rise in births in the coming year. Bank of America found that pregnancy test sales are up 13% YoY since 2020—a strong indication that there will be more births in 2022.

(Chart by Tradeswell)

With more people returning to offices, it comes as no surprise that sales of products in the Office Products category grew nearly 34% YoY in Q1 2022. According to a study by Microsoft, 50% of leaders say they already require or plan to require employees to return to in-person work full-time in the next year. Major companies, including Microsoft, Apple, Ford, and Wells Fargo, have all announced they will require employees to be back in the office on at least hybrid models—driving increased demand for office supplies.

(Chart by Tradeswell)

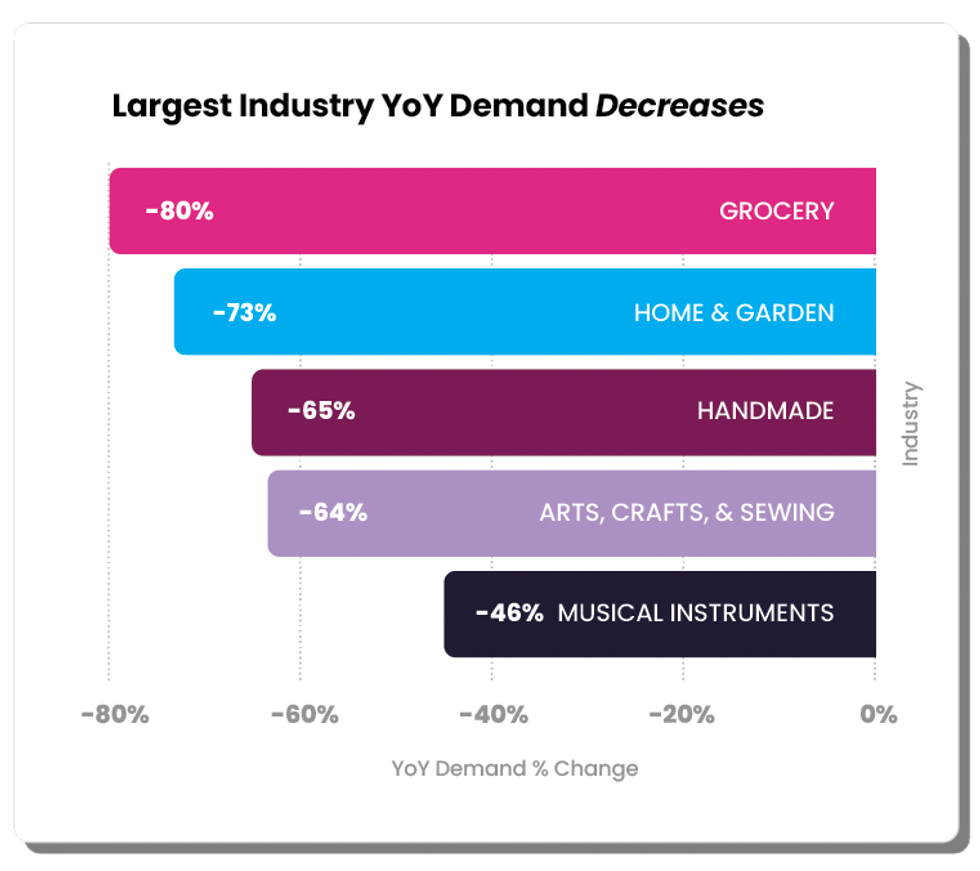

While many pandemic-driven online habits are here to stay, our findings suggest that shoppers are returning to physical stores for groceries.

Online consumer demand for groceries decreased 79% YoY. The availability of vaccines and drop in mask mandates have made shoppers feel more comfortable browsing for groceries in an aisle rather than from their couch. Another factor contributing to the drop in online grocery shopping is the increase in grocery prices due to the war in Ukraine. In-person shopping is less convenient, but it allows people to easily compare prices and products, and there’s no delivery and tip fee on top of the bill.

Remember when baking sourdough bread was all the rage? A survey by Lending Tree found that six out of ten Americans picked up a new hobby during the pandemic, but the return to pre-pandemic lifestyles has resulted in people abandoning these new activities. Arts, Crafts, and Sewing saw a 63% decline in consumer demand YoY, and Musical Instruments saw a 45% decline in consumer demand YoY. People are also spending less on Home and Garden products as they spend more time out of their homes.